This blog post outlines the key financial considerations for individuals facing redundancy in Ireland and who may have a pension with this employer.

Many employees ask us about what happens to their pension when they leave their current job. Job changes are more common today, and unfortunately, leaving pension savings behind with previous employers is also a frequent occurrence. When considering a job change, it’s crucial to understand the implications for your pension.

This can also be a good opportunity to sit down with your Financial Advisor and review how you are meeting your Retirement objectives or how you can improve on them. Contact me today if you wish to discuss your options and develop a strategy that aligns with your individual circumstances and financial objectives.

If you have been made redundant and have a pension in the Company, what are my options?

Defined contribution scheme –

Your pension benefits are managed and legally owned by the scheme’s trustees. When you leave your employment, your status within the scheme changes from ‘Active’ to ‘Deferred.’ Upon leaving your employment, you will receive a ‘Leaving Service Options letter’ or a ‘Pension Benefits Options Statement.’

This “Pension Benefits Options Statement” document will include important information such as:

The date you joined the scheme

The date you left

The value of your Pension

And finally set out your choices available to your particular situation upon leaving.

This is the starting point for assessing your options and it is therefore vital that you receive this document. You can request this document from the trustees of the scheme or alternatively if you sign a letter of authority I can undertake this work for you.

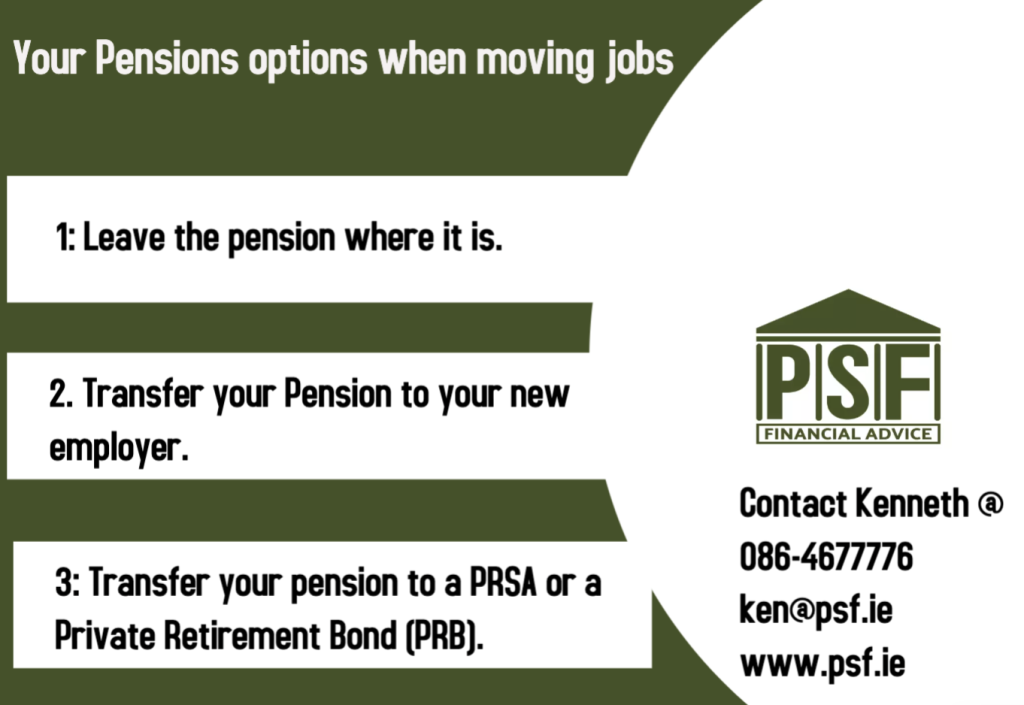

Essentially, you have three main options when leaving your company or employer.

Leave your Pension where it is (do nothing).

Transfer your Pension to your new employer.

Move your Pension into an account in your own name

Option 1: Do nothing – leave your pension with past/current employers

While it might be tempting to simply leave your pension pots with previous or current employers, it might not be the best option for you in the long run.

For starters, you need to make sure that each of your pension providers have your most up to date address and contact details so that you receive your personal benefit statements every year. Secondly, it’s extremely difficult to see the entirety of your pension benefits when you have multiple pots with different employers.

Finally, depending on the type of pension you held with your former company, it might not have a chance to grow any further, for instance if it’s been converted to cash rather than staying in the investment realm when you ceased employment.

Option 2: Transfer your old pension to your new employer

Not all pension schemes allow for this type of benefit transfer, for example the rules for transferring an existing fund into an employer’s PRSA are different to those for transferring into an executive pension.Transferring your previous pension benefits to your new employer is something that could certainly be worth considering if you envisage staying with the company for the long haul and the benefits of joining their scheme outweigh those of transferring to a Private Retirement Bond. If you move from the private sector into the public sector you can’t transfer a private pension in.

Option 3: Transfer your pension to a PRSA or a Private Retirement Bond (PRB)

Transfers the fund into an account in your own name: The pension scheme will allow you to transfer your pension fund from one arrangement to another. You can transfer the pension fund value into a Personal Retirement Savings Account or a Personal Retirement Bond (PRB) sometimes called a Buyout Bond. These accounts are in your own name, and you control the investment strategy.

Pros:

Full control over your pension and Investment decisions (the fund is owned by you personally).

Advice from Financial Advisor who can put together a tailored investment strategy (based on your attitude to risk) to help you reach your retirement goals and objectives.

Your accumulated rights are preserved (salary and service details recorded) giving you access to your tax-free lump sum entitlement and increasing your options to draw on retirement.

Move your PRB from one provider to another efficiently.

Your benefits can be taken from age 50.

Cons:

Annual Management Charges can be higher depending on the funds/asset classes you choose, your financial advisor will be able to offer advice on the charges.

Depending on your own personal circumstances, a Private Retirement Bond is also a popular choice for transferring a pension that you may have accumulated from working in the UK and keeping it under one roof alongside your other pots.A Private Retirement Bond also tends to give you more options at the time of retirement. Read separate article on PRB

Contact Kenneth to discuss your options

Previous PostStay-at-home parent role valued at annual salary of €57k – study

Next PostSecond hand home prices rose by 8.4% last year